HydroGraph: Why I'm on the Sidelines — and What Has to Change $HGRAF

Publicly Traded Companies Discussed in This Article: $HGRAF — HydroGraph Clean Power Inc. (CSE: HG / OTCQB: HGRAF) $SKYX — SKYX Platforms Corp. (NASDAQ: SKYX)

I first came across HydroGraph over two years ago. The CEO at the time had a distribution concept that I felt was a recipe for disaster. But I loved the graphene story so much that I wanted to go back and see if I could maybe influence a different direction for distribution.

That was when I met Kjirstin. She had replaced the previous CEO as interim CEO.

I asked her one question: "What is your plan for distribution?"

She came back with the perfect answer. I didn't have to try and influence a reconsideration. Kjirstin knew the answer because it made the most sense. That is when I got very excited about HydroGraph.

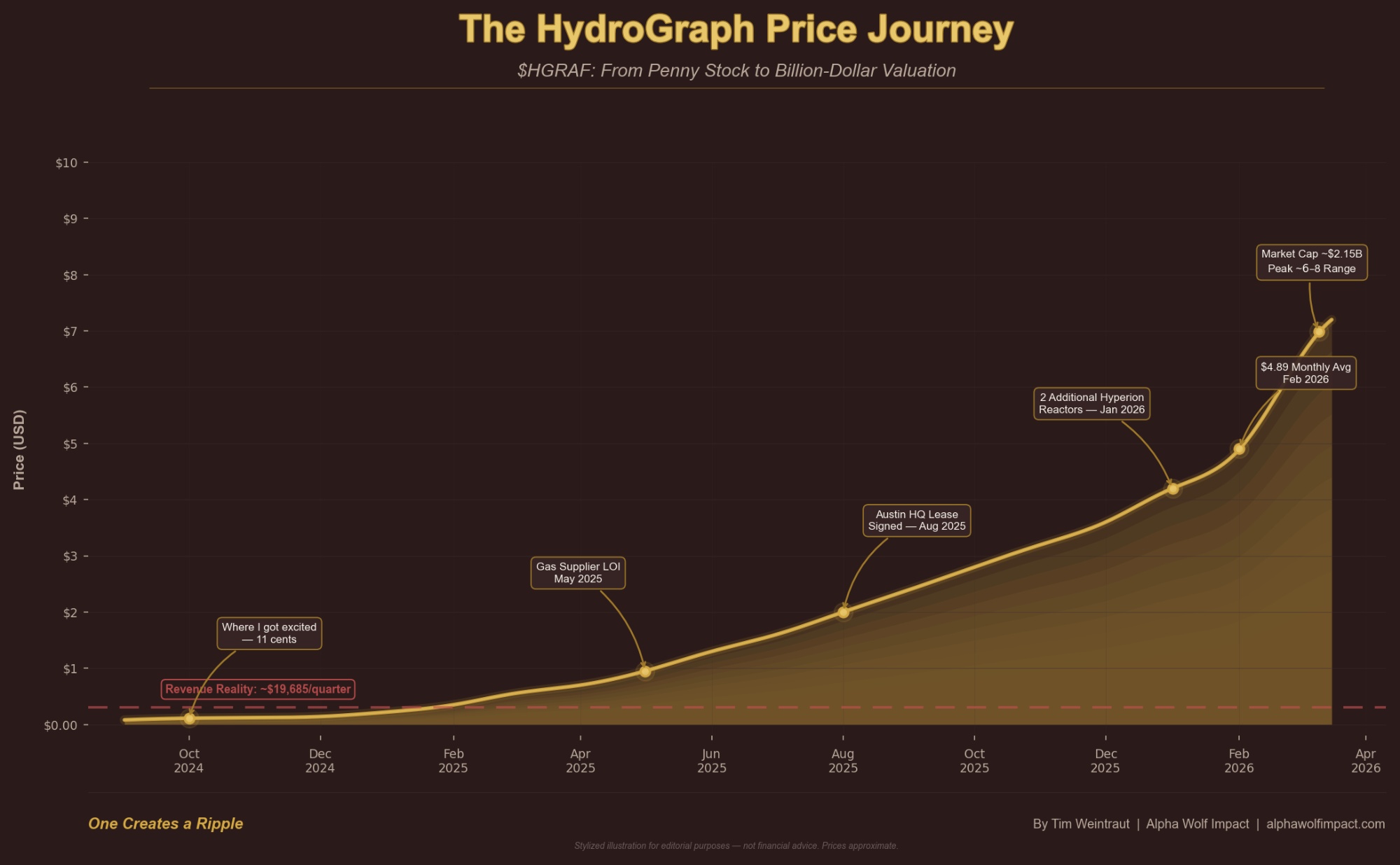

At the time, the stock was trading around 11 cents. The company was tiny, risky, and very early.

But I loved the idea:

Huge potential in batteries, concrete, coatings, and data centers.

A shot at becoming the first company to scale high-purity graphene production — with claimed near-100% SP2 bonding and high crystallinity — on a material that could literally make everything better.

200x stronger than steel

Harder than diamond

Flexible and translucent

1,000x more conductive than copper

Can make non-recyclable plastic recyclable

Enables better battery performance with fewer critical minerals

Cuts CO2 emissions from concrete

Can be used to filter drinking water

The possibilities are endless.

The Run — and the Reality Gap

That's life-changing for early holders. If you were in that sub-dollar zone, I'm genuinely happy for you.

But here's the problem — a massive gap has opened between the stock price and the underlying business:

No full-scale manufacturing facility. What they have is a 20,000 sq ft Austin HQ — basically doubling their space and giving them a control center. That's nice, but it's not 15 Hyperion reactors humming and shipping product.

The Texas production site is still a plan. It's tied to a gas supplier LOI announced in May 2025, marketed as a future home for 15 chambers and 350+ tons per year. But no site or supplier is publicly named, and timelines are aspirational.

No major exchange listing. Management has talked about redomiciling to the U.S. and uplisting to Nasdaq in "early 2026," but even their own communications admit no listing application is on file and the strategy is still under review.

Essentially zero revenue. The most recent quarterly filings show negligible sales — under $50,000 — against a net loss of $3.15 million for the quarter ending December 31, 2025.

In plain English: The market is pricing HydroGraph like the plant is funded, built, and producing. Reality says it's still a promise.

To be fair, not everything is just a promise. In February 2026, HydroGraph announced it received US EPA TSCA clearance along with UK REACH and EU REACH registrations — a genuine regulatory milestone that opens the door to commercial-scale graphene sales in the U.S., UK, and EU. That's real progress and it deserves to be acknowledged. But the EPA order comes with specified conditions, and the company has said final administrative steps are still required before full commercial commencement. Clearing regulatory hurdles is necessary — it's not the same as having customers, contracts, and revenue.

Recently a gentleman messaged me. He'd found one of my early interviews with Kjirstin. He loved the story. He started buying at 5–5.50.

And my stomach dropped.

I can't look at that follower — or any of you — and say nothing. Silence would be a lie.

[GRAPHIC: HGRAF Price Journey — visual showing the stock's run from $0.11 to ~$8 with key milestones annotated]

HydroGraph recently hired a new CFO, and in any serious company the CFO is deeply involved in up-listing, redomiciling, and building a real capital plan for major projects. That's a positive step and a necessary one if they're serious about Nasdaq and about building in Texas.

There are critics out there taking shots at Kjirstin's age, background, and résumé. I'm not joining that chorus.

What I can say from my own experience is this:

In some areas, she is wise beyond her years.

She genuinely cares about the science and about the scientist who made the discovery and developed the process. If you want to hear it in her own words, watch this moment from our interview where Kjirstin tells me what excites her most about HydroGraph. You can feel it.

HydroGraph is reportedly involved in 70-plus pilot programs, with 5–7 that could be genuinely transformational if they convert — not even counting whatever is going on with Dow or other large names.

I believe she wants to build something real and important. On that front, I will push back hard on people who just want to take lazy shots at her as a person.

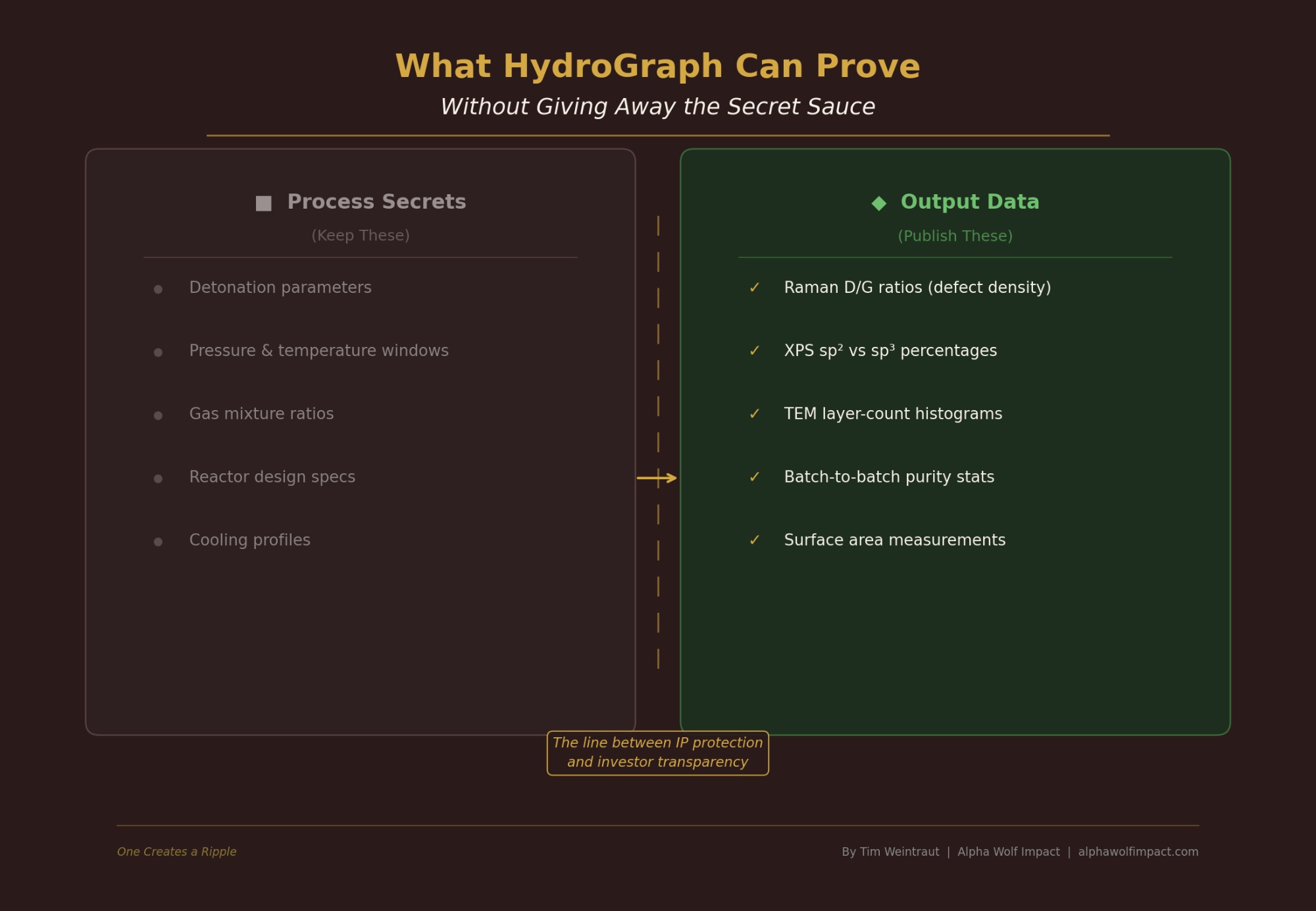

The SP2 / "Impossible Graphene" Debate

A short report claimed HydroGraph's talk about "100% SP2-bonded" and "100% crystalline" graphene is basically impossible. Strictly speaking, they're right about one thing: even the best methods rarely produce perfect, defect-free, single-layer graphene everywhere.

But I don't buy the blanket "it can't be done" story either.

With the right detonation process and tight control, you can get extremely high SP2 content, low defects, and a narrow layer-count distribution. The question isn't "Is it theoretically impossible?" The question is "Where does HydroGraph actually sit on that curve?"

The fix is simple and grown-up: data.

HydroGraph could shut down most of the scientific doubt tomorrow by releasing:

Third-party Raman data: D/G ratios (defect density) and 2D peak shape/position for dozens of batches.

XPS / REELS data: SP2 vs SP3 bonding percentages, again across many samples.

TEM images and histograms of flake thickness/size, so we see layer counts and morphology at scale.

Batch-to-batch stats on purity, surface area, layer distribution — not one cherry-picked run, but a real production spread.

Right now, we get big claims, badges, and general "verified" language, but not enough raw lab data for investors, engineers, or scientists to independently sanity-check the quality and scalability. If you want to build a material platform that changes the world, that's not good enough.

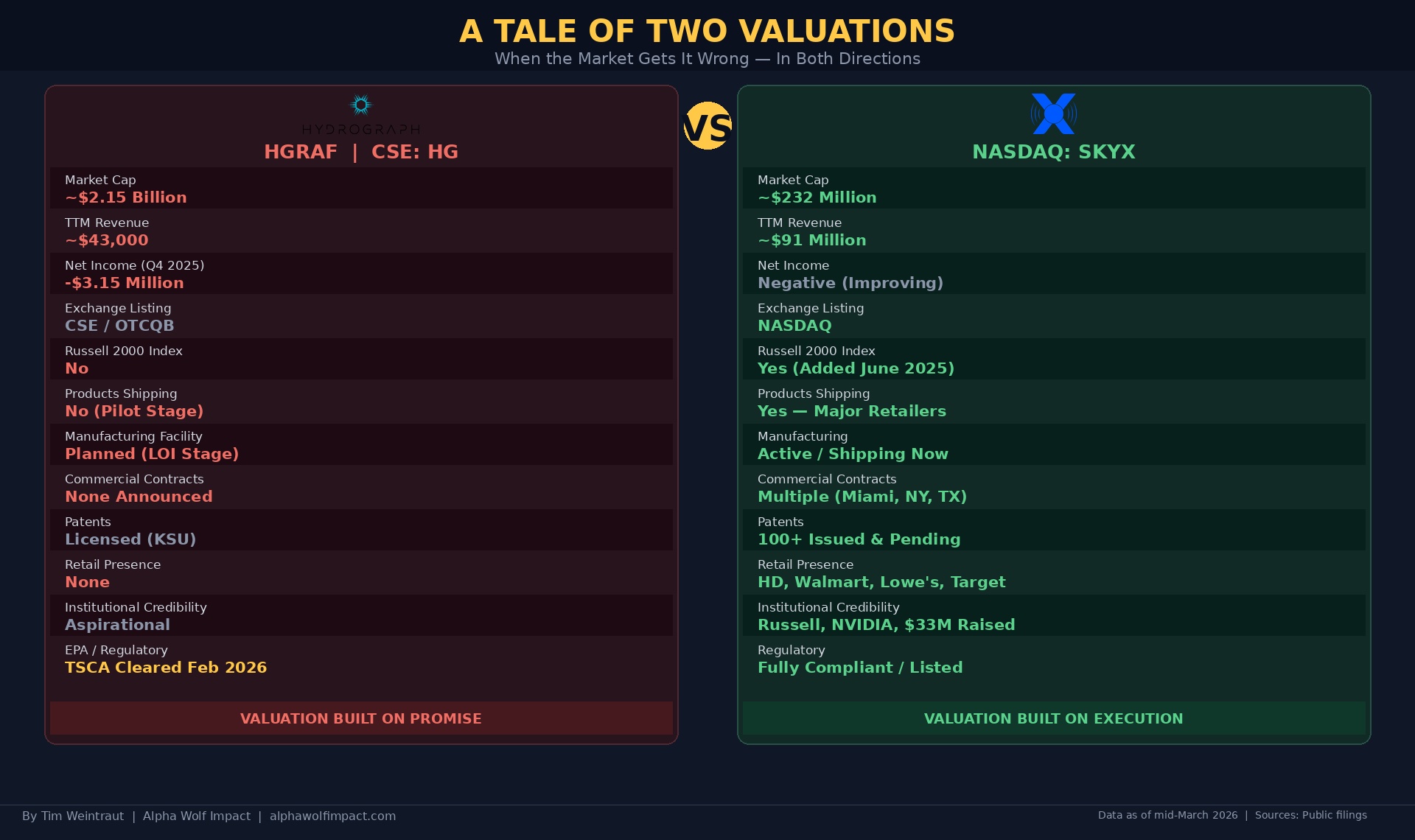

A Tale of Two Valuations: HydroGraph vs. SKYX

HydroGraph sits at roughly a $2.15 billion market cap as of mid-March 2026. Essentially zero revenue. No manufacturing facility online. No commercial contracts generating income. Not listed on a major exchange. The valuation is built entirely on promise and potential.

Now look at SKYX Platforms (NASDAQ: SKYX).

SKYX has a market cap of roughly $230 million — about one-ninth of HydroGraph's valuation. But here's what SKYX actually has:

~$91 million in trailing twelve-month revenue, with seven consecutive quarters of growth.

Products on the shelf at Home Depot, Wayfair, Target, Walmart, and Lowe's — right now, today.

Over 100 issued and pending patents globally on their advanced smart home plug-and-play ceiling platform technology.

Real commercial deployments — including a $3 billion Miami Smart City development where SKYX will deploy 500,000+ units of its advanced smart home technologies, agreements with Global Ventures Group for Middle East hotel and residential projects, collaborations with Forte Developments on luxury Miami high-rises, and a brand-new deal to supply 10,000 units for a New York apartment development.

A Nasdaq listing and Russell 2000 inclusion (added June 2025) — the kind of institutional credibility HydroGraph is still aspiring to.

A collaboration with NVIDIA through its Connect Program on AI-powered smart home integration.

A U.S. TAM that the company estimates at roughly $500 billion, with over 4.2 billion ceiling applications in the U.S. alone.

This isn't me bashing HydroGraph or pumping SKYX. This is me pointing out that the market can be wildly wrong in both directions at the same time. One company is being priced as if its entire future has already been delivered. The other is being priced as if its actual execution barely matters.

If you want a perfect case study in why valuation without context is meaningless — and why you need to do your own homework — this is it.

Fiduciary Duty and the Capital Question

With a multi-billion-dollar valuation on the screen, this company should be fully funded to build the Texas plant, redomicile, up-list, and meet higher reporting standards. That takes real money.

Instead, we've seen one equity raise around the 2-dollar range that brought in roughly $20M — helpful, but nowhere near what's needed for a large-scale plant and all the operational requirements. Management talks about big plans, but there is no public capex schedule that clearly bridges "here's what we have" to "here's a running, revenue-generating facility with 15 chambers."

It's also worth noting that shares outstanding have grown from roughly 187 million in mid-2024 to approximately 340 million today — meaning significant dilution has already occurred without a corresponding leap in operational capability. Shareholders are being diluted, but the plant still isn't funded.

At these prices, not raising enough capital to fully fund the build-out and de-risk the balance sheet is, in my view as a shareholder, a missed fiduciary opportunity.

If this stock trades back to 2 dollars — or 1 — and they haven't raised meaningful capital, the company and its shareholders are going to be in a very bad spot. The responsible move, in my view, would be to raise something on the order of $100M+ — enough to lock in the future while the market is giving them a gift.

Governance: Better, But Not Perfect

That said, I do have real concerns about one thing: She is both Chair and CEO.

I don't like that structure in any organization. It's the classic "who's watching the henhouse?" issue. In my opinion, separating the roles — or at least moving to a true lead independent director with real teeth — would send a strong signal on governance.

The Bambrough Question

I'm not accusing anyone of wrongdoing. But transparency matters, especially at this valuation, and there are legitimate questions that deserve straight answers.

He's been the loudest cheerleader:

- Publicly talking about buying 5% and later 10% of the company.

- Running long, bullish threads on X about HydroGraph being foundational and about people's cognitive biases making them miss 100x returns.

- Hosting interviews with Kjirstin and the chief scientist, framing this as the next great materials story.

That kind of excitement absolutely helped send the stock vertical.

But here's what I don't see:

So here's where I land on this:

When a multi-billion-dollar valuation is driven in large part by a highly vocal outside advocate whose real stake is hard to verify through public filings, smart investors should be on high alert.

Where I Stand — and What Has to Change

There are too many unknowns, too many big players kicking the tires — including serious government and defense-related conversations — for me to call this an obvious short. Anything could happen from here.

But the risk/reward has fundamentally flipped. When this was 11 cents, you risked 11 cents to maybe make a dollar or two. At these levels, a massive run on future promises, under-funded execution risk, and murky promotional incentives make this a setup where I cannot tell my community, "Load the boat."

For me to move from "pause" back to "engaged," I need to see:

Contracts — Real, meaningful commercial contracts announced — not just pilots and MOUs.

Facility — The manufacturing plant in Texas actually funded, built, and moving toward steady-state operation — not just an LOI and renderings.

Product at scale — Demonstration that they can produce high-purity graphene at the SP2 and crystalline quality they claim, at industrial volumes — not just lab or pilot runs.

Lab data — Independent, raw characterization data (the Raman, XPS, and TEM data I outlined above) published across many samples so scientists and investors can sanity-check the material.

Capital plan — A serious raise — in my view, $100M+ — that fully funds the build-out, redomicile, and uplist while this valuation window is open.

EPA and regulatory — Credit where it's due: HydroGraph received US EPA TSCA clearance and UK/EU REACH registrations in February 2026. That's a meaningful box checked. What remains is completing the final administrative actions required under the EPA order and demonstrating that regulatory authorization translates into actual commercial-scale production and sales — not just approval on paper.

That does not mean I hate the company, think Kjirstin is a bad person, or think HydroGraph can't win. It simply means too much has been priced in as if it has already happened.

If you've been in since 11 cents or under a buck, I think taking profits here — at least a meaningful chunk — is just smart risk management. Nobody ever went broke locking in a win.

If you're thinking about buying today because of my old interviews: Understand that my view has changed as new facts have come in. At these levels, I'm on the sidelines until those boxes are checked.

Let me leave you with this: I want HydroGraph to bring high-purity graphene to the world at scale because I believe it can improve many areas for humanity and provide a better quality of life. I am a huge fan of Dr. Sorensen and Kjirstin. I would like to see the entire team at HydroGraph knock it out of the park and make the world a better place.

When those boxes are checked, I'll happily revisit HydroGraph. Until then, I'm going to protect the people who put their trust in me.

I plan to keep a close eye on HydroGraph — and when the time is right, I'll be back with an update, whether that's another article or a video. The story isn't over. I just need the business to catch up to the stock price before I can tell you it's time to pay attention again

By Tim Weintraut

Alpha Wolf Impact | alphawolfimpact.com

Disclaimer: This article represents the personal opinion of the author and is not financial advice. The author is not a registered investment advisor. The author may hold positions in the stocks discussed and may buy or sell them at any time as new information becomes available. Past coverage of HydroGraph should not be interpreted as a current recommendation. This content is not paid promotion. Always do your own due diligence before making investment decisions.

Get Early Access & Exclusive Intel

The Watchlist. Full deep-dives. Monthly Wave Room. Early video access. Everything serious impact investors need — before the crowd catches on.

Free. Unsubscribe anytime. By subscribing you agree to our Privacy Policy.